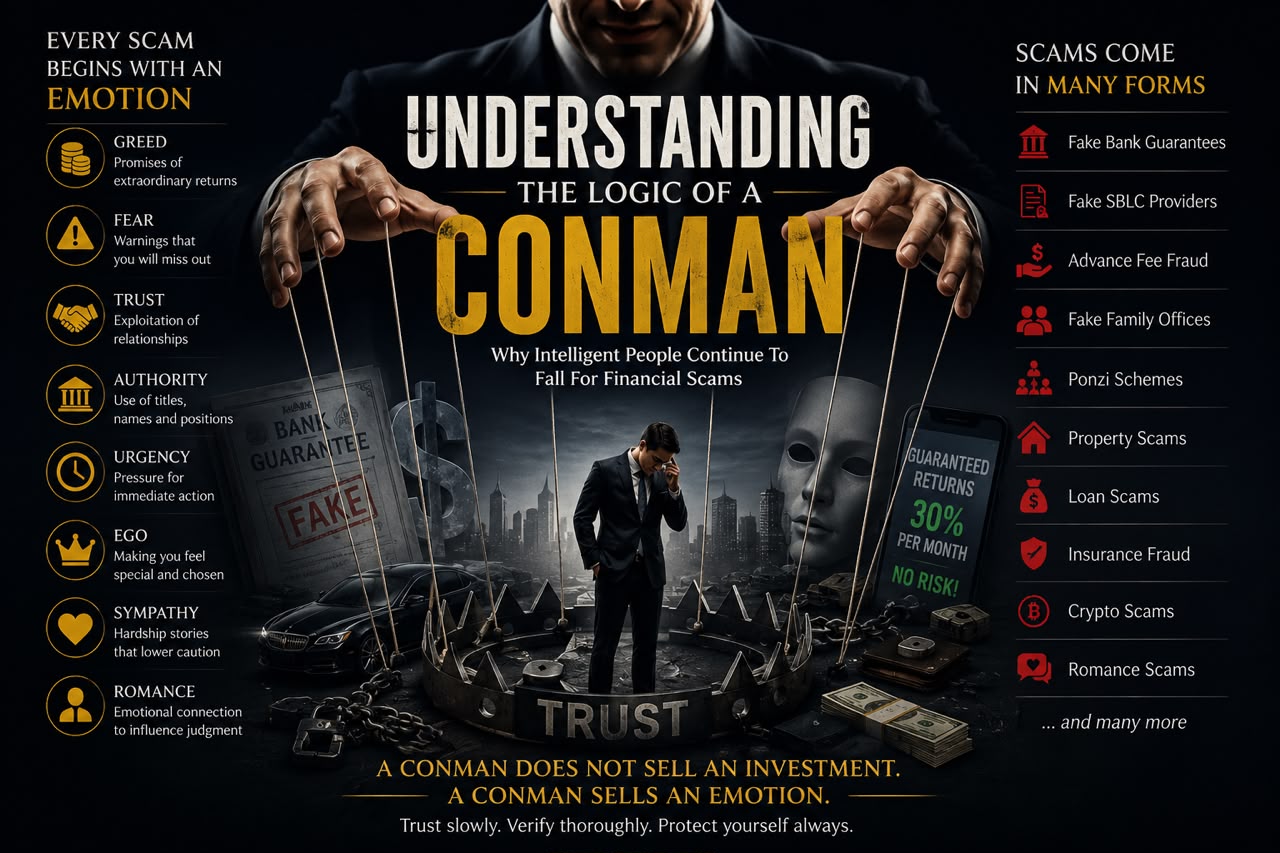

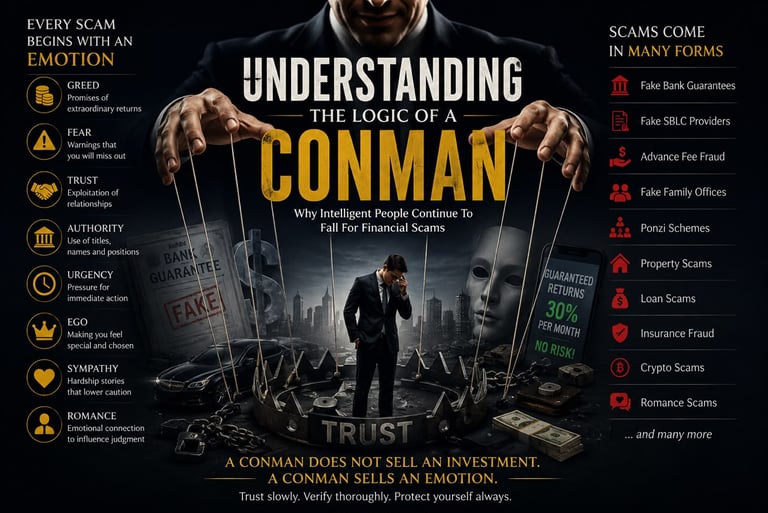

Understanding the logic of a conman

Drawing on nearly three decades of professional experience, Dr. Zarif Menon examines how fraudsters exploit human emotions rather than intelligence, offering practical insights to help readers recognise red flags and protect themselves from deception.

Dr Zarif Menon

6/30/202620 min read

Why Intelligent People Continue To Fall For Financial Scams

This article falls into the third category.

PART 1 — WHY I AM WRITING THIS ARTICLE

There are subjects that one writes about because they are interesting. There are subjects that one writes about because they are fashionable. And then there are subjects that one writes about because silence has become irresponsible.

In today's fast-moving economy, almost everyone is chasing something. Entrepreneurs are chasing capital. Investors are chasing returns. Business owners are chasing expansion. Professionals are chasing opportunities. Families are chasing financial security. Ordinary people are chasing a better life. In the middle of all this movement, urgency and ambition, a dangerous class of people has learned how to position themselves very cleverly: the conman.

The conman is not new. He has existed in every generation, every culture and every economy. What has changed is the speed, sophistication and reach of modern deception. Today, a fraudster can operate across borders, use professional-looking documents, create artificial credibility through social media, hide behind corporate structures, misuse the names of banks and government bodies, and reach victims through WhatsApp, email, LinkedIn, Telegram, Zoom meetings and polished websites.

Fraud has become faster. Deception has become more presentable. Lies have become better dressed.

This article is not written merely to discuss conmen in the capital raising sector. Capital raising is certainly one of the areas where fraudsters thrive because people seeking funding are often under pressure, hopeful and vulnerable. But fraud is not limited to capital raising. It exists across investment schemes, property deals, commodity trading, banking instruments, cryptocurrency, insurance, loan arrangements, gold transactions, oil and gas facilitation, forex trading, private placements, family office introductions, charitable appeals, romance scams, religious affinity groups and even ordinary business partnerships.

The reason I am writing this article is also personal.

Since 1998, I have spent more than twenty-eight years working with entrepreneurs, business owners, investors, financiers, advisers and intermediaries across various sectors and jurisdictions. I have seen good people lose money. I have seen businesses damaged. I have seen families divided. I have seen friendships destroyed. I have seen honest consultants treated with suspicion simply because dishonest people came before them and poisoned the well of trust.

I have also experienced deception myself. I say this openly because it is important for readers to understand that being cheated is not always a sign of stupidity. In many cases, people are not cheated because the fraudster is smarter than them. They are cheated because the fraudster found a way to enter through trust, emotion, relationship, sympathy, urgency or personal vulnerability.

There have been situations where I trusted people because of relationships. I trusted them because of shared history. I trusted them because of introductions. I trusted them because I believed they had personal issues, financial pressures or genuine difficulties. I trusted them because I wanted to help. In hindsight, the weakness was not intelligence. The weakness was confidence placed in the wrong person.

That is why this article matters.

Too many people still believe that only foolish people get scammed. That is simply not true. Doctors get scammed. Lawyers get scammed. Accountants get scammed. Bankers get scammed. Business owners get scammed. Politicians get scammed. Religious leaders get scammed. Educated families get scammed. Experienced investors get scammed. People with decades of business experience get scammed.

A good conman does not begin by attacking your intelligence.

He begins by studying your emotions. He studies what you want. He studies what you fear. He studies what you lack. He studies what you hope for. He studies who you trust. He studies how quickly you want results. He studies your ego, your desperation, your ambition and your kindness. Then he designs the deception around that emotional entry point.

This is why I believe the defining truth of this article is simple: a conman does not sell an investment; a conman sells an emotion.

If readers understand only that one sentence, they will already become more difficult to deceive.

The purpose of this article is not to make people paranoid. Paranoia is not wisdom. Suspicion alone is not intelligence. If we become suspicious of everyone, then genuine business becomes impossible. The real objective is discipline. Trust, but verify. Listen, but question. Explore, but document. Be open-minded, but never careless.

In a world where fraud has become professional, awareness must also become professional.

PART 2 — THE LOGIC OF A CONMAN

To understand fraud, we must first understand the mind of the fraudster.

A legitimate entrepreneur asks: How do I create value? A legitimate adviser asks: How do I solve a problem? A legitimate investor asks: How do I manage risk and create return? A legitimate consultant asks: How do I assist my client responsibly?

A conman asks a very different question: How do I extract value without creating any real value?

That is the foundation of the conman's logic.

The conman is not interested in building. He is interested in taking. He is not interested in long-term credibility. He is interested in short-term extraction. He is not interested in accountability. He is interested in disappearance, delay, confusion or plausible denial.

The conman's business model is simple: maximum reward, minimum effort and minimum accountability.

This is why fraudsters often avoid clarity. Clarity creates accountability. They prefer vague language, complicated explanations, impressive but unverifiable documents, international terminology, unofficial confirmations, mysterious channels, unnamed principals, private allocations, confidential mandates, secret investor groups and time-sensitive opportunities. The more difficult something is to verify, the more room the conman has to operate.

A conman rarely begins with the lie itself. He begins with positioning.

First, he creates credibility. He may claim to know bankers, royal families, politicians, billionaires, fund managers, family offices, oil traders, gold suppliers, sovereign funds or institutional investors. He may show photographs with important-looking people. He may use logos. He may forward documents with letterheads. He may refer to private meetings. He may mention countries and institutions that sound impressive. He may speak confidently about procedures that most victims do not fully understand.

Second, he creates exclusivity. The victim must feel selected. The opportunity must feel rare. The victim is told that not everyone has access. This makes the victim feel important and reduces the natural instinct to question too much.

Third, he creates urgency. The victim must act before thinking too deeply. Funds must be transferred quickly. Documents must be signed immediately. The allocation will close. The principal is waiting. The bank officer is available only today. The window is closing. Urgency is one of the most powerful weapons in fraud because it shortens the time available for due diligence.

Fourth, he creates dependency. The victim is made to believe that only the conman can open the door. Only he has the connection. Only he understands the process. Only he can speak to the principal. Only he can arrange the funding. Only he can secure the allocation. Once the victim believes access depends entirely on the conman, the conman controls the victim.

Fifth, he creates excuses. When money is paid and results do not arrive, delays begin. Compliance issue. Bank issue. Holiday issue. Legal issue. Document issue. Technical issue. Regulator issue. Principal travelling. Funds blocked. New requirement. Another fee. Another certificate. Another approval. Another step.

A real transaction becomes clearer over time. A fraudulent transaction becomes more complicated over time.

That is one of the most important distinctions readers must remember.

Example one: the fake capital arranger. A business owner urgently needs USD 10 million for expansion. A so-called intermediary claims to have direct access to a Middle Eastern investor. He asks for an upfront processing fee to prepare the file, arrange meetings and secure the investor's commitment. The business owner pays because the opportunity sounds credible. Weeks pass. The investor is always travelling, the documents are always under review, and the business owner is eventually asked for another payment to solve a new issue. The funding never arrives.

Example two: the fake bank instrument provider. A client is told that a standby letter of credit or bank guarantee can be arranged quickly through a private banking channel. The provider uses banking terminology confidently, sends draft documents and asks for a commitment fee. When verification is requested directly with the issuing bank, excuses begin. The bank officer is confidential. The transaction is private. Verification can only happen after payment. These are dangerous signs. Genuine bank instruments do not require secrecy from legitimate verification.

The logic of the conman is always the same. Create belief. Create urgency. Create dependency. Extract money. Delay accountability. Repeat.

PART 3 — EVERY SCAM BEGINS WITH AN EMOTION

Most people think scams begin with documents, investments or business proposals. They do not. Scams begin with emotions.

The document is merely the costume. The proposal is merely the stage. The real weapon is emotional manipulation.

The first emotion is greed. Greed does not always mean evil. Sometimes it simply means wanting more than what is reasonable. Fraudsters understand this very well. They know that when people hear about unusually high returns, their caution often weakens.

Example one: a scheme promises 20% to 30% monthly returns through forex, crypto, gold trading or private placement programmes. The victim may know the return sounds unrealistic, but the possibility of fast profit overwhelms caution.

Example two: an alleged pre-IPO opportunity is presented as exclusive access before a company lists publicly. The victim is told that insiders are quietly accumulating shares and that the price will multiply after listing. No proper prospectus exists, no regulated adviser is involved, and yet greed makes the opportunity feel too good to miss.

The second emotion is fear. Fear is extremely powerful because it creates urgency.

Example one: the victim is told that if he does not invest now, he will lose the opportunity forever. The fear of missing out becomes stronger than the need to verify.

Example two: a business owner is told that his company will collapse unless he urgently secures a particular funding arrangement. The fraudster positions himself as the only solution and uses fear to force quick payment.

The third emotion is trust. Trust is perhaps the most dangerous entry point because it disables suspicion.

Example one: a family friend introduces an investment scheme. The victim trusts the relationship and assumes that no one close to the family would intentionally cause harm.

Example two: a respected member of a religious or community group recommends a financial opportunity. Because the recommendation comes from a trusted circle, the victim does not conduct proper independent verification.

The fourth emotion is respect for authority. Fraudsters love authority because people are conditioned to respect titles, uniforms, official language and institutional names.

Example one: a person claims to represent a government-linked programme or development fund and offers special financing assistance. The documents appear official, but the email address, verification process and payment instructions do not match any proper institutional procedure.

Example two: a fake banker or former banker claims to have internal access to loan approvals. The victim assumes that banking language equals banking authority. It does not.

The fifth emotion is urgency. Urgency is the enemy of due diligence.

Example one: a commodity buyer is told that a gold allocation or fuel allocation must be secured within 24 hours by paying a reservation fee. No proper verification is allowed because the window is supposedly closing.

Example two: a victim is told that funds must be transferred before the end of the banking day to secure participation in a private investment programme. The pressure is designed to prevent independent advice.

The sixth emotion is ego. Fraudsters know that people enjoy feeling important.

Example one: a business owner is told that he has been specially selected by an international investor group because of his reputation. The flattery lowers his guard.

Example two: an entrepreneur is invited to an exclusive closed-door opportunity supposedly reserved for high-net-worth individuals. The victim feels privileged and does not want to appear inexperienced by asking basic questions.

The seventh emotion is sympathy. Kind-hearted people are often vulnerable to sympathy-based manipulation.

Example one: a friend claims to have a temporary cashflow problem and asks for a short-term loan, promising repayment within days. The story changes repeatedly after funds are given.

Example two: a person claims medical emergency, family tragedy or business disaster and uses emotional pressure to obtain money without documentation.

The eighth emotion is romance or emotional attachment.

Example one: online romance scams involve months of emotional grooming before the victim is asked for money due to a supposed emergency, business problem or blocked bank account.

Example two: a business relationship gradually becomes emotionally personal, and once emotional dependency is created, the victim is persuaded to fund deals, pay fees or cover losses.

This is why fraud education must begin with emotional awareness. When emotions rise, verification must increase. When urgency rises, caution must increase. When trust becomes personal, documentation becomes even more important.

A conman studies emotions because emotions often open doors that logic would have kept closed.

PART 4 — THE CAPITAL MARKETS: A FRAUDSTER'S PARADISE

The capital markets and the wider capital raising environment are particularly attractive to fraudsters because the sector naturally involves large numbers, complicated structures, international parties and specialised terminology.

Most ordinary business owners do not fully understand bank instruments, private placements, sovereign funds, family office procedures, escrow mechanics, securities regulations, trade finance, project finance or institutional due diligence. Fraudsters exploit this knowledge gap.

Complexity becomes their hiding place.

One common area is advance fee fraud.

Example one: a company seeking USD 50 million is told that an investor has approved the funding in principle, but the company must first pay legal, administrative, compliance or arrangement fees. Once paid, another fee appears. Then another. The promised funding never materialises.

Example two: a borrower is told that a loan facility has been secured from an overseas lender. A commitment letter is issued, but before disbursement, the borrower must pay insurance fees, activation fees or transfer taxes. Genuine lenders normally deduct legitimate fees from proceeds or document them transparently. Fraudsters demand upfront payments into questionable accounts.

Another common area is fake bank guarantees and standby letters of credit.

Example one: a provider claims that he can arrange a bank guarantee from a top international bank without collateral or proper banking due diligence. This alone should raise suspicion because real banks do not issue serious instruments casually.

Example two: the victim receives a draft instrument with impressive language, SWIFT references and bank details. However, direct bank verification is discouraged. The fraudster claims that verification can only happen after payment. That is a major red flag.

Fake family offices are also increasingly common.

Example one: a person claims to represent a wealthy family office in Europe or the Middle East, offers large funding, and asks for facilitation costs before any formal due diligence process begins.

Example two: a fake family office uses a website, luxury branding and vague references to global investments, but has no verifiable principals, no regulated advisers, no proper corporate history and no transparent investment process.

Fake sovereign wealth fund or government fund representations are also dangerous.

Example one: an intermediary claims to have access to sovereign capital for infrastructure projects but cannot provide any verifiable mandate, official channel or authorised correspondence.

Example two: a fraudster misuses the name of a real national fund or government agency and claims to operate through a confidential representative. Genuine sovereign or government-related institutions do not normally operate through secret private channels demanding upfront fees.

Commodity allocation scams are another major area.

Example one: a seller claims to control large gold allocations at discounted prices, but cannot provide verifiable proof of title, refinery documentation, assay reports, storage confirmation or proper transaction procedures.

Example two: a fuel or crude oil allocation is offered at highly attractive pricing. The buyer is pressured to pay commitment fees, logistics fees or allocation fees before legitimate proof of product is established.

Yield enhancement and private trading programmes are among the most dangerous fraud categories because they sound sophisticated.

Example one: a victim is told that funds will be placed into a high-yield bank trading programme generating extraordinary weekly returns. The explanation is filled with references to platforms, screens, traders and blocked funds, but no regulated documentation exists.

Example two: the investor is told that only wealthy insiders can access these programmes and that secrecy is required. In reality, secrecy is used to prevent the victim from seeking independent verification.

The capital markets attract fraudsters because victims often want fast funding or fast returns. The fraudster provides the story they want to hear. That is why serious capital work must always involve verification, legal review, regulatory awareness and disciplined documentation.

PART 5 — FRAUD IN TRADITIONAL FINANCE

Although modern scams often involve cryptocurrency, digital platforms or cross-border transactions, traditional finance has always had its own forms of fraud. The methods may change, but the underlying logic remains the same.

Ponzi schemes remain one of the most famous examples.

Example one: early investors receive returns not from real profits but from money contributed by later investors. This creates the illusion of success and encourages existing investors to reinvest or introduce friends.

Example two: a so-called investment club promises consistent monthly dividends regardless of market conditions. When investors ask how profits are generated, the explanation is vague. As long as new money enters, the scheme appears healthy. When new money slows down, the structure collapses.

Property scams are equally damaging.

Example one: investors are sold units in a development that has not obtained proper approvals, land rights or financing. The marketing material is beautiful, but the legal foundation is weak.

Example two: the same property or land interest is sold to multiple parties through manipulated documents, nominee arrangements or unclear titles. Victims only discover the problem when enforcement or registration becomes necessary.

Loan scams are common because people seeking loans are often under pressure.

Example one: a business owner receives a loan approval letter from an alleged lender but must pay processing fees before disbursement. After payment, new requirements appear and the loan never arrives.

Example two: individuals with poor credit are promised guaranteed personal loans by online agents. They are asked for stamp duty, insurance or activation fees. Once paid, communication stops.

Insurance fraud also affects both individuals and businesses.

Example one: a person is sold a fake policy by someone pretending to represent a legitimate insurer. Premiums are collected, but no valid coverage exists.

Example two: policy replacement fraud occurs when an agent persuades a client to cancel an existing policy and buy a new one, not because it benefits the client, but because the agent earns commission.

Investment-linked product abuse is another area where victims may not realise the risk.

Example one: a product is presented as safe savings when it actually carries market risk, fees and surrender penalties.

Example two: elderly or financially inexperienced clients are pushed into complex products they do not understand, simply because the salesperson is chasing commission.

Crypto and digital asset scams have grown because technology creates both excitement and confusion.

Example one: a fake crypto exchange shows rising account balances on screen, but withdrawals are blocked until the victim pays taxes or unlocking fees.

Example two: a token project promises guaranteed future value, celebrity endorsement or exchange listing, but has no real utility, no credible team and no transparent governance.

Forex and trading scams continue to deceive many.

Example one: a trader claims to generate fixed monthly profits with no losses. Real markets do not work that way.

Example two: victims are shown manipulated trading dashboards where profits appear real until they attempt withdrawal.

Traditional finance teaches us an important lesson: fraud does not require new technology. It only requires trust, complexity and insufficient verification.

PART 6 — THE RELATIONSHIP ATTACK VECTOR

Some of the most painful frauds do not begin with strangers. They begin with people we know, people introduced by those we trust, or people who slowly become familiar enough to bypass our normal caution.

This is what I call the relationship attack vector.

A fraudster who approaches as a stranger faces resistance. A fraudster who arrives through a friend faces less resistance. A fraudster who becomes a friend may face almost no resistance at all.

This is why relationship-based fraud is so dangerous.

The victim does not feel that he is dealing with a transaction. He feels that he is helping someone, supporting someone, trusting someone or joining someone in an opportunity. Once a transaction becomes personal, professional discipline often weakens.

Example one: a long-time friend introduces a business opportunity and says, 'Brother, I would never bring this to you if I did not believe it was genuine.' The victim trusts the relationship more than the documents. Later, when the deal collapses, the friend claims he was also misled.

Example two: a person slowly builds personal closeness by sharing problems, family difficulties and emotional stories. After trust is formed, he asks for financial assistance, short-term advances or support for a business arrangement. The victim helps out of compassion, not commercial logic.

Fraudsters also borrow credibility from respected people.

Example one: they mention the names of politicians, businessmen, religious leaders, bankers or royalty to create the impression of legitimacy, even when those people have no real involvement.

Example two: they attend high-profile events, take photographs with important personalities, and later use those photographs to imply endorsement or partnership.

Affinity scams operate in similar ways.

Example one: a fraudster targets members of the same religious community, knowing that shared faith reduces suspicion.

Example two: a fraudster targets business associations, alumni groups or ethnic communities, using shared identity as a substitute for proper verification.

This is why I have learned that the closer the relationship, the stronger the documentation must be. This may sound harsh, but experience teaches hard truths.

When strangers deceive us, we feel foolish. When trusted people deceive us, we feel wounded. Relationship-based fraud hurts more because it steals more than money. It steals memory, friendship, dignity and trust.

The lesson is not to stop trusting people. The lesson is to stop confusing trust with exemption from verification.

If a proposal is genuine, verification will strengthen it. If verification destroys it, then the proposal was never strong to begin with.

PART 7 — WHY SMART PEOPLE GET SCAMMED

One of the greatest myths about fraud is that only foolish people become victims.

This myth is dangerous because it makes intelligent people overconfident. They assume their education, experience or professional status protects them. It does not.

Intelligence protects against some forms of ignorance. It does not automatically protect against emotional manipulation.

A doctor may understand medicine but not private banking instruments. A lawyer may understand contracts but not commodity trade procedures. An engineer may understand systems but not investment regulation. A successful entrepreneur may understand his own industry but not structured finance. A banker may understand banking but still be vulnerable to friendship, ego or desperation.

Fraudsters exploit the gap between intelligence and specialised knowledge.

They also exploit confidence.

Example one: an experienced business owner believes he can quickly recognise fraud. Because of this confidence, he skips independent checks and relies on instinct. The fraudster flatters his experience and encourages him to move quickly.

Example two: a professional investor assumes he is too sophisticated to be deceived. The fraudster presents a complex structure full of technical language and secrecy. The investor does not ask basic questions because he does not want to appear uninformed.

Smart people also get scammed because they are often busy. Busy people delegate trust. They rely on summaries, introductions and assurances. Fraudsters know that busy people may not have time to verify every detail.

Example one: a business owner asks an assistant or introducer to handle preliminary checks, but the introducer lacks the knowledge to detect red flags.

Example two: a wealthy individual relies on a trusted acquaintance who appears confident but has no actual authority or expertise.

Another reason smart people get scammed is hope. Hope is not foolish. Hope is human. A struggling business owner hopes for funding. An investor hopes for returns. A family hopes to recover losses. A lonely person hopes for companionship. A desperate borrower hopes for approval.

Fraudsters do not need to defeat intelligence when they can amplify hope.

This is why fraud prevention must be based on systems, not ego. Systems protect us when emotions are high. Verification protects us when trust is strong. Written documentation protects us when memory becomes selective. Independent advice protects us when our own judgement becomes compromised.

This is why fraud prevention must be based on systems, not ego. Systems protect us when emotions are high. Verification protects us when trust is strong. Written documentation protects us when memory becomes selective. Independent advice protects us when our own judgement becomes compromised.

PART 8 — RED FLAGS EVERYONE SHOULD REMEMBER

Fraud rarely arrives wearing a sign that says fraud. It arrives dressed as opportunity, friendship, urgency, exclusivity or rescue.

Therefore, every person should learn to recognise red flags.

The first red flag is guaranteed high returns.

Example one: any scheme promising fixed monthly returns far above normal market rates with little or no risk should be treated with extreme caution.

Example two: trading programmes that promise profits regardless of market conditions are usually hiding either misrepresentation or outright fraud.

The second red flag is urgency.

Example one: you are told to transfer money today or the allocation will disappear.

Example two: you are pressured to sign documents before your lawyer or adviser can review them.

The third red flag is resistance to due diligence.

Example one: when you ask for verification, the other party says, 'Do you trust me or not?' That is emotional manipulation.

Example two: when you request direct confirmation from a bank, investor, seller or authority, excuses begin.

The fourth red flag is unclear identity.

Example one: the person claims to represent a powerful principal but refuses to provide proof of mandate.

Example two: corporate documents show recently formed entities with no track record, no substance and no verifiable operations.

The fifth red flag is payment to unrelated parties.

Example one: fees are requested into a personal account rather than a properly documented company account.

Example two: funds are requested to be paid to a third party who is not named in the agreement.

The sixth red flag is overcomplexity.

Example one: the explanation contains excessive jargon but no simple commercial logic.

Example two: every direct question receives a longer and more confusing answer rather than a clearer one.

The seventh red flag is hostility towards questions.

Example one: the other party becomes offended when you ask for documents.

Example two: you are accused of being negative, fearful or disrespectful because you want verification.

The eighth red flag is inconsistency.

Example one: names, dates, amounts, bank details or procedures keep changing.

Example two: the story changes depending on who is asking the question.

The ninth red flag is secrecy.

Example one: you are told not to speak to lawyers, banks or advisers because the opportunity is confidential.

Example two: you are told that written confirmation cannot be provided until payment is made.

The tenth red flag is emotional pressure.

Example one: the person uses friendship, religion, family or loyalty to discourage proper verification.

Example two: the person creates guilt by saying that your delay will cause him loss, embarrassment or failure.

Whenever red flags appear, slow down. A genuine opportunity can survive questions. A fraudulent opportunity usually cannot survive verification.

PART 9 — THE COST TO SOCIETY

Fraud does not only damage the victim. It damages society.

When a person loses money to fraud, the financial loss is only the beginning. Trust is damaged. Confidence is damaged. Relationships are damaged. Families are damaged. Businesses are damaged. Communities are damaged.

A victim may become suspicious of everyone. A business owner may refuse genuine assistance in the future. An investor may avoid legitimate opportunities. A consultant may struggle to convince clients that honest professionals still exist. This is the wider cost of fraud.

In the capital raising and financial advisory world, fraud has created a heavy burden for genuine practitioners. Honest consultants now spend considerable time proving that they are not like the dishonest ones. Genuine advisers must overcome suspicion created by people they never met and scams they never participated in.

This is unfair, but it is the reality of today's market.

Example one: a business owner previously cheated by a fake funding arranger may reject a genuine advisory process because he assumes all advisers are the same.

Example two: an investor previously exposed to fake documents may become overly defensive and miss a legitimate opportunity because trust has been damaged.

Fraud also damages legitimate capital flow. When scams become common, real investors become more cautious. Banks become stricter. Advisers become more defensive. Due diligence becomes heavier. Transactions take longer. Good businesses suffer because bad actors polluted the environment.

This is why fraud awareness is not merely a personal protection issue. It is an economic issue.

Every scam increases friction in the marketplace. Every fraudulent scheme makes genuine business harder. Every dishonest intermediary increases the burden on honest professionals. Every fake opportunity weakens confidence in real opportunities.

The damage is not limited to money stolen. The deeper damage is trust destroyed.

And once trust is destroyed, rebuilding it takes years.

PART 10 — FINAL REFLECTIONS

After all these years, I have reached a simple conclusion.

Trust is valuable. Verification is essential.

We cannot build business without trust. But we also cannot survive in business with blind trust. The solution is not suspicion. The solution is discipline.

Trust slowly. Verify thoroughly. Ask questions. Document everything. Seek independent advice. Do not be ashamed to pause. Do not be pressured by urgency. Do not let friendship replace paperwork. Do not let emotion replace judgement. Do not let greed silence common sense.

If someone is genuine, they will respect your need to verify. If someone becomes angry because you ask reasonable questions, that anger itself is information.

A conman does not sell an investment. A conman sells an emotion.

He sells greed as opportunity. He sells fear as urgency. He sells trust as access. He sells ego as exclusivity. He sells sympathy as obligation. He sells complexity as sophistication. He sells delay as process. He sells silence as confidentiality.

But truth does not fear verification.

A genuine opportunity becomes stronger under scrutiny. A genuine adviser welcomes clarity. A genuine investor expects due diligence. A genuine transaction can be explained simply. A genuine relationship does not collapse because documents are requested.

Fraudsters rarely break down doors. More often, they are invited inside.

They enter through trust, hope, ego, fear, desperation, kindness or ambition. That is why awareness is so important.

My message to readers is not to stop trusting people. Without trust, life becomes empty and business becomes impossible. My message is to trust with wisdom.

Be kind, but not careless. Be open, but not naive. Be ambitious, but not greedy. Be helpful, but not blind. Be respectful, but not silent when questions must be asked.

In today's world, the best protection against fraud is not intelligence alone. It is discipline. It is patience. It is verification. It is the courage to walk away when something does not feel right, even if the opportunity appears attractive.

Money lost can sometimes be recovered. Trust, once broken, is far more difficult to rebuild.

Therefore, let us learn before we lose. Let us verify before we commit. Let us question before we transfer. Let us protect ourselves, our families, our businesses and our communities from those who profit from deception.

Because in the end, the greatest defence against a conman is not fear.

It is awareness.

Contact

Dr. Zarif Menon

Founder, President & CEO

Pacific Alliance Group (PAG)

Phone

admin@zarifmenon.com

admin@pacificalliancegroup.my

+44 7888 438570 (UK)

+60 16 666 7898 (Malaysia)

+62 877 7999 7898 (Indonesia)

© 2026. All rights reserved.